Quick Answer: How Indian Residents Can Secure a UAE Golden Visa Via Dubai Property

The UAE Golden Visa has become one of the most sought-after residency programs for Indian investors, especially those looking to diversify assets and gain a foothold in Dubai’s thriving property market.

For Indian residents, the Liberalised Remittance Scheme (LRS) provides a compliant route to invest in UAE real estate and secure a 10-year renewable Golden Visa—opening doors to tax-efficient living, family sponsorship, and unmatched global mobility.

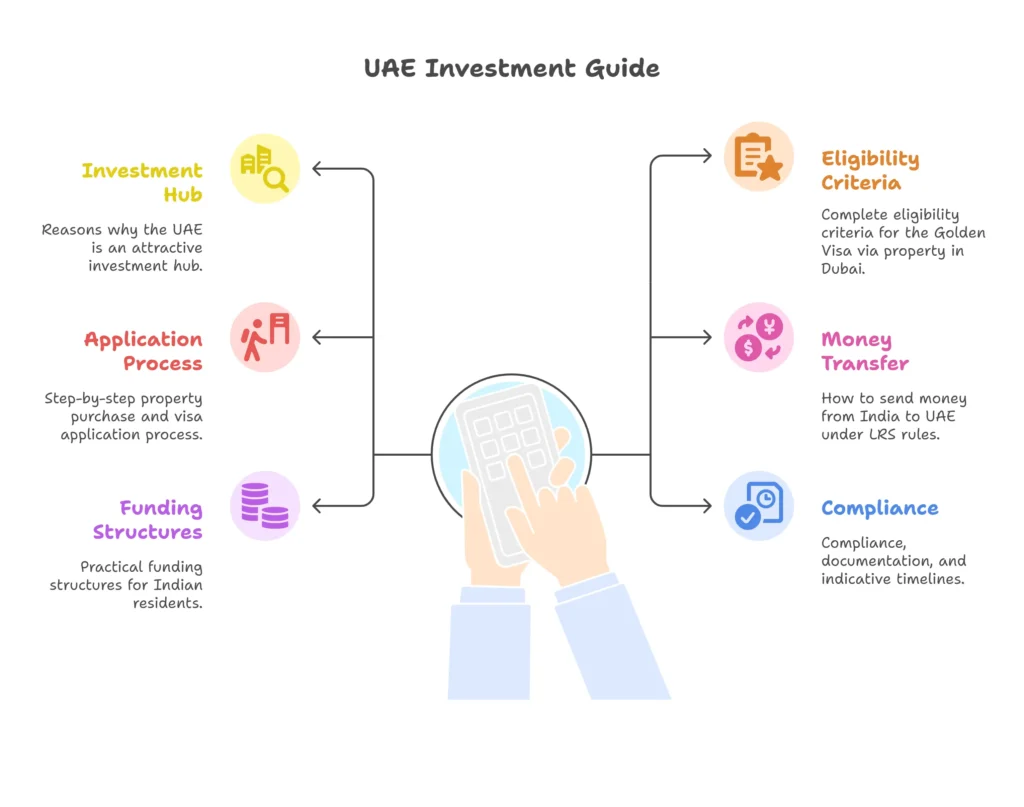

This comprehensive 2025 guide will walk you through:

- Why the UAE is an attractive investment hub

- Complete eligibility criteria for the Golden Visa via property in Dubai

- Step-by-step property purchase and visa application process

- How to send money from India to UAE under LRS rules

- Practical funding structures for Indian residents

- Compliance, documentation, and indicative timelines

1. Snapshot: Why UAE & What the Golden Visa Gives

Why UAE?

Dubai offers:

- A tax-free environment (no personal income tax)

- World-class infrastructure and lifestyle

- Strategic location connecting Asia, Europe, and Africa

- A stable real estate market with high rental yields

What the Golden Visa Offers

Duration: 10-year renewable residency (self-sponsored)

Privileges:

- Live, work, and study anywhere in the UAE without a local sponsor

- Sponsor spouse, children (no age limit), parents, and unlimited domestic staff

- No local partner required for business

- Long-term stability for families and investors

Exemption from 6-Month Entry Rule

Most UAE residence visas require you to enter the UAE at least once every 6 months to keep the visa active. Golden Visa holders are exempt:

- Stay outside UAE for over 6 months without cancellation

- Ideal for Indian investors who prefer part-time UAE residence

- Sponsored dependents under your Golden Visa also enjoy this exemption

2. Golden Visa via Property – Eligibility & Documents (Dubai Focus)

Core Eligibility for Real Estate Investors:

- Own property (single or multiple) with a total purchase value ≥ AED 2 million

- Properties can be combined to meet the AED 2M threshold

- Eligible for both ready and off-plan properties, as well as mortgaged purchases (documentation required)

Required Documentation (Typical):

- Passport (valid)

- Current UAE visa & Emirates ID (if applicable)

- Title deed(s) or off-plan purchase contract(s) (Oqood)

- Health insurance

- Medical test results

- Biometrics

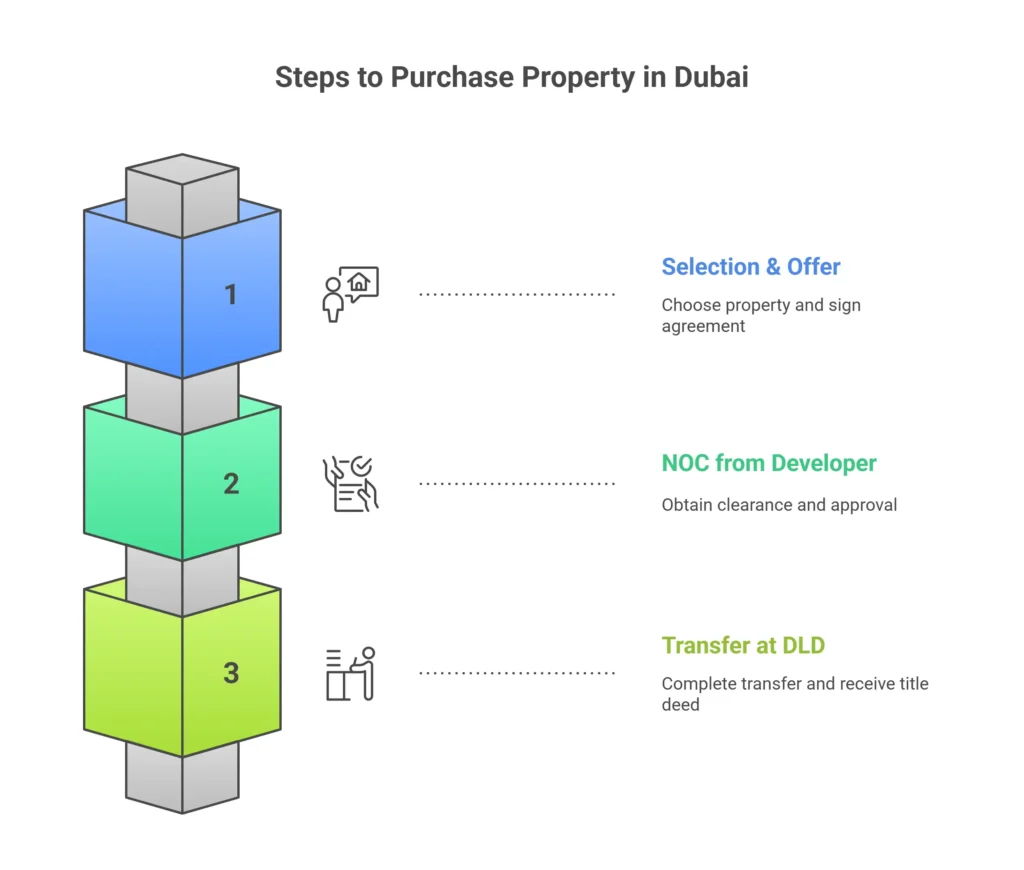

3. Property Purchase in Dubai — Step-by-Step

Step 1: Selection & Offer

- Choose the property (ready or off-plan)

- Sign RERA Form F (MoU) with seller or Sales Purchase Agreement (SPA) for off-plan

Step 2: NOC from Developer

- Confirms all dues cleared and transfer approval granted

- Typical NOC Fee: AED 500–5,000

Step 3: Transfer at Dubai Land Department (DLD) Trustee Office

- Pay applicable fees and complete transfer

- Receive e-Title Deed immediately after successful registration

Typical Fees:

| Fee Type | Amount |

| DLD Transfer Fee | 4% of purchase price |

| Trustee Office Fee | AED 4,000 + 5% VAT (≥ AED 500k) / AED 2,000 + VAT (< AED 500k) |

| Title Deed/Admin | AED 250–580 |

| Mortgage Registration | 0.25% of loan amount + ~AED 290 admin |

| Broker Commission (if applicable) | ~2% of price |

4. After Transfer: Applying for the Golden Visa

Process Overview:

- Submit application through Land Department / ICP / GDRFA

- Undergo medical test and biometrics

- Apply for Emirates ID

- Receive Golden Visa

Processing Time: Typically 3–5 working days from application submission

5. Sending Money from India to UAE — Liberalised Remittance Scheme (LRS)-Compliant Banking Channel

What is LRS?

The RBI’s Liberalised Remittance Scheme allows an Indian resident to remit up to USD 250,000 per financial year (April–March) for permitted purposes, including purchase of overseas property.

Purpose Code for Property Purchases:

- S0005 – “Indian investment abroad – real estate” (reported via Form A2 by your bank)

Bank Documentation (Typical):

- Form A2 + FEMA declaration

- PAN and KYC

- Proof of source of funds

- SPA or invoice from seller/developer

- Banks check your available LRS limit before SWIFT transfer

Pooling of Funds:

- Immediate relatives can combine LRS limits to purchase the same property, ensuring each remitter complies with LRS

TCS (Tax Collected at Source) — India (Effective April 1, 2025):

- Threshold increased to ₹10 lakh per FY

- For “any other purpose” (includes property), TCS at 20% applies on the amount above ₹10 lakh

- Claim TCS credit in your Indian Income Tax Return

Pro Tip:

Large transactions are often structured over multiple financial years and/or across eligible family members to stay within limits. Some investors set up a UAE company to purchase property—this requires a separate legal process.

6. Practical Funding Structures for Indian Investors

Example Structures:

- All Cash (Staggered): Split payments over multiple FYs under USD 250k per person limit; secure Golden Visa after full payment & title deed issuance

- Joint Ownership: Combine ownership between spouses/relatives to reach AED 2M requirement; ensure clean audit trail with matching remitter and owner names

7. Our Role & Responsibilities

We provide end-to-end guidance, including:

- Property shortlisting, price verification, and selection

- Structuring deals (cash, mortgage, off-plan)

- Coordinating with DLD Trustee for smooth transfer

- Preparing Golden Visa application file (ICP/GDRFA)

- Managing timelines to align property transfer and visa issuance

- Assisting with LRS remittances, FEMA compliance, and Indian Income Tax obligations

- Full registration at Dubai Land Department and title deed issuance

8. Compliance & Record Keeping

For India:

- Maintain Form A2, SWIFT copy, SPA, title deed, UAE bank credit proofs, and TCS payment receipts

- Report foreign property in Schedule FA of Indian ITR, if applicable

For UAE:

- Keep title deed, payment receipts, mortgage contract (if any), Golden Visa approval, and Emirates ID details

9. Indicative Timeline (Cash Purchase, Ready Property)

| Week | Process |

| 1–2 | Property selection, offer signing, initial LRS remittance |

| 2–4 | NOC from developer, DLD Trustee transfer, e-Title Deed issuance |

| 4–6 | Golden Visa application, medical, biometrics, Emirates ID issuance |

FAQ- UAE Golden Visa via Dubai Property for Indian Residents

Can I combine multiple properties to meet the AED 2M threshold?

Yes. Both ready and off-plan properties can be aggregated if the total registered value is equal to or above AED 2 million, allowing investors with multiple smaller assets to still qualify for the Golden Visa.

Are mortgaged properties eligible for the Golden Visa?

Yes, as long as the total property value meets the AED 2 million eligibility criteria and you provide the mortgage-related approvals and payment proof from the bank or developer.

Do I need to visit the UAE every 6 months?

No. Golden Visa holders are exempt from the usual UAE residency rule that requires residents to enter the country every 6 months to maintain their visa status.

Can I pool LRS with my family members?

Yes, immediate family members can combine their Liberalised Remittance Scheme (LRS) allowances to purchase property, provided each member follows the Reserve Bank of India’s LRS rules and documentation requirements.

Conclusion

Securing the UAE Golden Visa via Dubai property is a strategic investment move for Indian residents seeking long-term residency benefits, tax efficiency, and international lifestyle flexibility. With careful LRS-compliant structuring, the process is straightforward and achievable—whether through staggered cash payments, joint ownership, or mortgage financing.

Our specialised team ensures full compliance in both India and UAE, smooth property acquisition, and successful Golden Visa issuance, making your UAE investment journey seamless from start to finish.

No comment yet, add your voice below!